Report on carbon-free steel production: Cost reduction options and usage of existing gas infrastructure

EnergyVille/VITO, at the request of the European Parliament Think Tank, has evaluated the potential and limitations of the future role of hydrogen in decarbonising the iron and steel industries.

The steel sector is one of the most challenging sectors to decarbonise and has recently received special attention owing to the potential use of low-carbon hydrogen (green and blue) to reduce its fuel combustion and process-related carbon emissions. This report addresses concerns that might arise while evaluating the potential and limitations of the future role of hydrogen in decarbonising the iron and steel industries. The report provides a comprehensive overview of current technical knowledge, (pilot) projects and road maps at national and EU level.

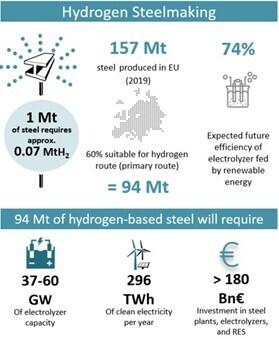

In Europe the production of crude steel is currently at around 157 Mt, accounting for 4 % of GHG emissions. Approximately 60 % (94 Mt) of total European steel production originates from the coal-based blast furnace/basic oxygen furnace (BF/BOF) route and is more suitable for the hydrogen direct reduction route (H-DRI). The authors of this study estimate that 94 Mt of ‘green steel’ would require approximately 37-60 GW of electrolyser capacity, producing approximately 6.6 Mt of hydrogen per year. As a reference, the EU hydrogen strategy aims to have 40 GW of electrolyser capacity installed within the EU by 2030. The authors estimate that these electrolysers would consume approximately 296 TWh of green electricity per year; as a reference, Germany produced in total 176 TWh of green electricity in 2020.

Currently, the existing hydrogen transport infrastructure is one of the main bottlenecks in the transition to sustainable hydrogen use in the EU. EU gas transmission owners are conducting studies and tests on which components of their infrastructure can be reused for transporting hydrogen. A most likely approach will be the creation of so-called hydrogen valleys to serve and connect regions of energy-intensive industrial clusters.

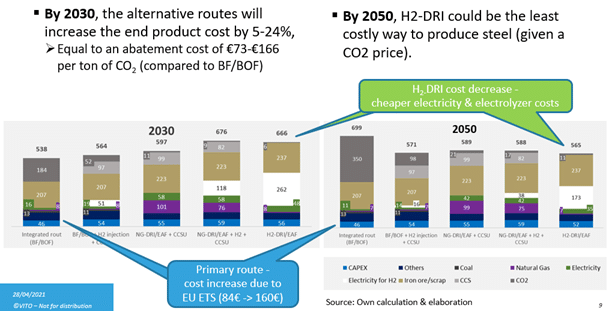

Comparing the expected cost per ton of steel among the potential production routes, the authors’ calculation shows that by 2030, the innovative routes will increase the end product cost by a premium of 5-24%, with an abatement cost of €73-€166 per ton of CO2, compared with the integrated route BF/BOF[1].

[1] The calculation assumes for all production routes an EU ETS of 84 Euro/ton of CO2 in 2030. (for 2050 price comparisons see Figure 15).

The authors’ team would also refer to the AidRES project – advancing industrial decarbonisation by assessing the future use of renewable energies in industrial processes – which was launched in January 2021 and which will create a database for the main Energy Intensive Industries in Europe, including current and future energy and feedstock needs, and map out renewable energy needs in high spatial resolution.